The Efficient Market Hypothesis (EMH), proposed first by Fama (1965a,b) has been the common assumption of the field of economy for the greater part of the 20th Century. It presupposes the economically active individual to be a rational actor who processes information rapidly and efficiently, and that stock prices reflect all existing information. Implicit in the view was that investors are rational, and operate using all information available, rather than relying on intuition. Although some of the more extreme views of the EMH (such as investors processing information near instantaneously) have been diluted, in many ways modern finance builds off the core presupposition of rational actors utilizing all of the information that they have available to them.

This view however has not gone unchallenged. A growing body of literature and commentary is drawing attention to the limited cognitive capacities of individuals and the frequent interference of emotion and intuition. The Behavioural Finance perspective espouses the bounded rationality of individuals and their frequent recourse to heuristics, especially in the face of information overload. Since the 2007-8 financial crisis, psychologists and economists have been drawing attention to these shortcomings, from individuals to households and even to large, well-structured and equipped organizations. This brief article will attempt to provide a survey of this literature in exploring the psychological shortcomings which contribute to boom/bust cycles.

Although the cognitive limits and emotional impulses of individuals are among the chief causes of these boom/bust cycles, as will shortly be discussed, they manifest themselves differently in different sorts of organizations given the different pressures and goals of those collectives. As such, the first part of this survey will concern financial and governmental organizations, whereas the latter part will examine households.

Organisations

Organisations frequently have an outsized effect on the direction of economic developments. Compared with individuals or with households, financial organisations have clear hierarchies, goals almost entirely within the domain of finance, and have vastly more resources allotted to these goals. Shefrin (2010) provides a comprehensive analysis the psychological pitfalls which contributed to the 2007 financial crisis, taking UBS, Standard & Poor’s, and the Norwegian town of Narvik as examples where these pitfalls manifested themselves.

@Natelu – View of Hong Kong

Risk Seeking

One of the greatest superordinate factors which both contributed to the financial crisis was risk and its mismanagement. As Shefrin (2010) notes, UBS, an investment banking firm that securitized mortgages, began to take higher risks, and although there was much focus on the returns they sought, they increasingly violated the basic financial tenet that expected return and risk have a positive relation. S&P similarly became more risk neutral, if not risk-seeking, when it came to adjusting criteria for the rating of CDOs (Lucchetti, 2008).

In both cases, they showed this increased tolerance for risk as a result of falling behind in the competition. People seem to frame their decisions in terms of gains and losses with reference to a reference point, and according to internal communication at those organizations, that reference point was their competitor’s success. Resultantly, they felt that they were operating out of the domain of losses (insofar as missed opportunities, especially those lost to a competitor, constitutes a loss), which ultimately lead them to take greater risks to escape this sense of loss, a phenomenon which Shefrin (2010) labels reference-point induced risk seeking. Further studies into the domain of risk seeking indicates that individuals may view the same sum of money differently when it comes to gambling (Koop & Johnson, 2010; Peng, Miao & Xiao, 2013). Peng, Miao & Xiao (2013) found that individuals feel the loss of 100 Yuan as allowance (or ante) more acutely than the loss of the same amount as gambling wins. Thus, it is possible that as they UBS and S&P felt they were closing the gap, they became even more comfortable with risk as they felt they had made gains, which were stored in different mental accounts.

Loss Aversion

Directly tied with risk seeking then, it is only natural to discuss loss aversion. While until recently, the value of loss and reward of the same magnitudes were considered to be equal (Ricciardi, 2008), the psychological literature suggests otherwise. According to Kahneman & Tversky (1979), people are more concerned with losses and gains, and investors will assign greater weight to the avoidance of a loss than the achievement of gain. Tversky & Kahneman (1986; in Shefrin, 2009) hold that this translates to differential outcomes in risk-taking behaviour. Consider the following:

A. A sure $2400

B. 75% chance of $0

25% chance of $10,000

C. A sure $7,500 loss

D. 75% chance of losing $10,000

25% chance of losing $0

In most cases, individuals opt in Choice task 1 for option A (deemed to be a safe bet), however, in Choice task 2, opt for option D, the higher risk option which nevertheless offers a slim hope of the avoidance of any loss. Thus, it seems that individuals do not psychologically weigh gains and losses in the same manner, and further that these are carriers of value in and of themselves. Thus, risk behaviour differs in the face of uncertain gains versus uncertain losses, making individuals risk-averse in the domain of gains, and risk-seeking in the domain of losses (Shefrin, 2009).

This difference in participant choice illustrates how, when faced with a certain gain or a higher but uncertain alternative, people will routinely opt for the more assured gain with the lower risk. However, when it comes to losses, people will routinely opt to take a risk with as low as 20% success rate if there’s even a hope of avoiding a loss. Furthermore, as Barberis & Huang (2001) notes, individuals seem to be loss averse in terms not broadly defined, such as by overall worth or sum, but by narrowly defined gains and losses (say of a particular stock).

Conservatism Bias

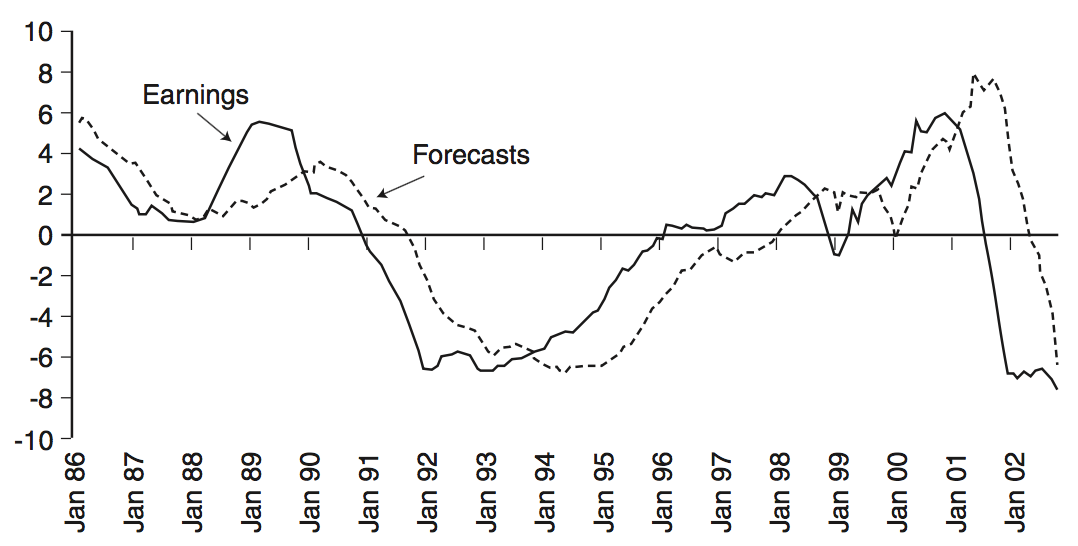

Pompian (2012; 2015) describes conservatism bias as “a mental process in which people cling to their prior views or forecasts at the expense of acknowledging new information”, or similarly, the tendency to weigh historical information, such as the past performance of a stock more heavily relative to new information. As Hirschleifer (2001) notes, asset prices are in a constant state of flux, and the processing of new information and the updating one’s beliefs is cognitively costly affair.

From Dresdner Kleinwort Wasserstein, 2002, in Pompian, 2012: Analysts are exceptionally good at telling you what just happened.

This manifests itself in a number of ways. Investors often cling to forecasts more than to emerging data points, and when they to react to new data, they are slow to do so. Shefrin (2009) states that the AIG financial products division, which insured the mortgage securities through default credit swaps exhibited conservatism bias in its assumption that historical mortgage rates would continue to be valid.

Groupthink

Groupthink is the psychological tendency to conform to group consensus and expectation (Janis, 1982). As Shefrin (2009) describes, in high-pressure environments, exemplified in their analysis of S&P, individuals show groupthink behaviour by minimizing the conflict in their internal discussions and reaching a hasty conclusion about how to rate collateralized debt without any thorough testing or meaningful discussion of the assumptions. Similarly, UBS managers exhibited groupthink by not sufficiently challenging one another in regard to how their businesses were developing, especially in light of the magnitude of the changes they were making in terms of risk.

Group dynamics play themselves out differently, depending on the circumstance, and the shouldn’t be seen as a blanket condemnation of cooperation or group efforts. As noted by Bang & Frith (2017), in situations where the task requirements are clear and there is an abundance of information, group work often maximises positive results, with members correcting their peers by reference to clearly available information. However, when the task at hand is broader, the criteria more nebulous, and judgement based more on intuition or estimation, and the information lacking group dynamics work in the opposite direction. With members unable to base their dissent on clear information, they show a tendency to conform to group consensus, believe others have better knowledge and dissent far less. Bang & Frith (2017) give financial bubbles as an instructive example of such behaviour, where individual traders may be uncertain about the true value of assets, and therefore infer that others buying to be indicative of its value, and using this in lieu of any other information.

Confirmation Bias

The confirmation bias is a subconscious search to find information that confirms a prior decision and avoids information containing contrary evidence (Lord et al., 1979). According to Shefrin (2009) both the US Securities and Exchange Commission (SEC) and UBS showed signs of confirmation bias in their conduct. The former displayed this bias by ignoring the early warning signs of a housing bubble whereas the latter showed confirmation bias, as when they began to experience losses on their inventories of mortgage backed securities in early 2007 “their risk team did not implement any additional risk methodologies.” In effect, they ignored signs of a troubled housing market and displayed an overconfidence in their capacity to deal with problems which might arise.

Overconfidence & the Above Average Bias

Overconfidence can be defined as the miscalculation of probabilities, biased in favourable terms (Glaser & Weber, 2010). Alternatively, overconfidence can be defined as a particular form of miscalibration, where the assigned probability that those answers are correct exceeds the true accuracy of those answers.

It is one of the most widely studied phenomena (Daniel & Titman, 1999), and in this instance, would lead investors to believe they were invulnerable to specific risky activities or overestimate their ability to cope. They draw attention to the small Norwegian town of Narvik, who enacted a strategy of borrowing money generated by their local power plant and investing the proceeds into securities that included among them collateralized debt obligations. Comments by the mayor indicated an optimistic bias about their capacity to handle the risks in a situation they did not quite comprehend. As Rosen (2009) points out, the investors were also overconfident given they overestimated the precision of their beliefs about the securities, thinking that the higher yields weren’t due to the higher associated risk but rather that other investors’ default risk estimates were incorrectly high.

Households

Households are typically considered victims of recessions, and indeed, they typically operate from far less secure positions than large organizations, with far fewer resources to buttress them and far fewer tools with which to navigate and make decisions. They are also frequently the victim of predatory lending practices which often take advantage of their limited financial literacy. However, the behaviours of households also contribute to economic downturns, and while individual households do not contribute much, the large number of households means that the effects of common errors are amplified.

@ragingwind – Warsaw Old Town, Warsaw, Poland

Extrapolation Bias & Representativeness

Extrapolation Bias refers specifically to the belief that the future will likely follow a similar pattern to what is known of the past. One might not know how the stock market will be in the future but have an idea of how it was last year. As Nofsinger (2010) states, people will transfer characteristics of the known to the unknown if the two are deemed to be closely related enough. In the present context, it means that households are not aware of or excited about an investment until after it has seen a surge in price and value, and believe that this surge in value will continue. It also means that if they experienced good returns on investment one year, they are likely to believe this will continue into the next. They are, in short, late getting in and late getting out, buying when during boomtime and selling during bust.

Providing broad support for this view, Malmendier & Nagel (2011) conducted a study using the Survey of Consumer Finances from 1960 to 2007, investigating the effect of individual experiences of macroeconomic shocks on financial risk taking. Their results indicate that recent personal experiences exert an outsized influence on personal decisions. Furthermore, market experience early in one’s life affects one’s dispositions to stock market participation, and the generation into which one was born has an effect on preference and belief formation as it relates to trust in financial institutions, stock markets and policy preferences. They note that following the recessions of the 1970s-80s, young people’s stock market returns were dominated by low returns, leading to decreased participation. They also demonstrated that higher experienced stock returns are associated with more optimistic beliefs about future stock returns, suggesting that while individuals do attempt to learn from their experiences, they do not do so using all ‘available’ historical data.

Groupthink

Groupthink also seems to affect households, though perhaps in a different fashion than it does large organizations. While in the latter case, groupthink manifests itself in a more explicit fashion, with group members minimizing their dissent in the face of high pressure and clear social hierarchies, in the case of households it seems to arise less conspicuously. Shiller (2008) holds that one of the main ways groupthink manifested itself in relation to the 2007-8 crash was the pervasive and largely unchallenged view of housing as investment. Families were seeing real estate as a reliable and secure investment, believing housing prices would reliably continue to increase.

@vivalaveronica – One in A Million

Culture & Shifting Stigmas

As Nofsinger (2012) notes, attitudes towards indebtedness have drastically changed in the past few decades, and it is increasingly socially permissible and normal to carry high levels of debt, with the household debt rising from $7 trillion to $13.6 trillion in the period from 2000-2007, and naturally accompanying the higher levels of debt are also higher levels of bankruptcy – but such an increase in the rates of bankruptcy subsequently leads to a loss of stigma and shame surrounding bankruptcy (Buckley & Brinig, 1998). While in contemporary western culture, stigmatization is seen as a negative, no-fun-allowed attempt to shame individuals, stigma acts as a social restraint mechanism for risky behaviours to curb and mitigate damage to community. When considered from a historical perspective, the loss of stigma surrounding interest, debt and bankruptcy certainly lay a strong groundwork for households acting in riskier ways, taking on more debt than they might be able to handle, and acting with less restraint as one more social psychological barrier is removed. In turn, this would lead to households to take on more debt than they can handle and default in large numbers, causing substantial losses to lenders.

Financial Literacy & Cognitive Limitations of Households

It has been observed that, in the face of complex and byzantine contracts and decisions whose effects unfold and shift over time, households typically employ simplifying heuristics and shorthands at the best of times (Duhaime & Schwenk, 1985), both in their decisions through active discounting of certain pieces of information as well in how they perceive such information in the first place (Nofsinger, 2012). This natural tendency of humans in the face of information overload can somewhat be mitigated by sophisticated financial instruments and general financial literacy, however these are frequently lacking for households and individuals (Lusardi & Mitchell, 2007; Hilgert Hogarth & Beverly, 2003). For example, Rooij, Lusardi & Alessie (2011) developed two modules for De Nederlandsche Bank (DNB) Household Survey to measure financial literacy in relation to stock market participation. Their results found that most respondents to the survey had a basic grasp on financial concepts such as interest compounding and inflation, however few went beyond these. For example, there was a marked lack of knowledge regarding risk diversification, which in turn lead to skewed perceptions of risk. Furthermore, these individuals were more likely to turn to friends and family for financial advice.

By and large, this leaves individuals & households to reckon with these complex problems themselves, at which point they are hamstrung by their cognitive limitations. Firstly, a low ability to perform simple mathematical calculations is associated with less savings (McArdle et al, 2010), poorer understanding of credit (Lusardi & Tufano, 2008), and less retirement planning (Lusardi & Mitchell, 2009). Gerardi, Moetta & Meier (2010) conducted a highly comprehensive survey to specifically investigate subprime borrowers’ financial literacy and cognitive ability in 2008, matching individual-level measures to micro-level datasets containing extensive information of mortgage characteristics and payment histories. Their results show a strong significant association between a numerically ability (which they subsume as an aspect of financial literacy) and mortgage delinquency (such as late payments or foreclosure), and holds up even when other socio-economic and demographic control variables are entered into the analysis. Their findings indicate that for individuals, the cause of their delinquency has less to do with excessively risky behaviour (as in the case of larger organizations, noted by Shefrin (2009) and Nofsinger (2012)), but more to do with limited numerical ability and its effects over time. Such borrowers were no more likely than others, in Gerardi et al.’s (2010) analysis, to be pushed towards unfavourable contract terms or predatory lending However, the authors do note that about 60% of subprime mortage defaults happened within two years of origination, and thus that the relationship between limited numerical ability and unfavourable contract terms is unclear.

As Agarwal & Mazumder (2013) states, in the case of choosing an investment portfolio, “an investor must synthesize a wide range of information concerning economic conditions and the past performance of various assets, accounting for transactions costs, asset volatility, and covariance among asset returns. This task requires memory, computational ability, and financial sophistication.” (p.1). Indeed, Kamleitner, Hoetzl et al. (2012) has found that consumers weigh a few salient aspects of a potential loan more heavily than others, with borrowers struggling to integrate down payments, repayments and overall loan durations (Herrmann & Wrickle, 1998). Counterproductively, he presence of such complexity and of psychological stress cause borrowers and households to focus even further on a limited number of salient items (Kahn & Baron, 1995; Leith & Baumeister, 1996). Even more worryingly, borrowers seem to linearize, and thereby underestimate functions containing exponential terms, such as those in instalment credit, when assessing them intuitively (Stango & Zinman, 2006; 2009), thus leading to those households to borrow more and save less.

Comparisons and Conclusions

It thus appears that households and more financially sophisticated organizations contribute differentially to financial recession. This is largely unsurprising – larger financial organizations have vastly different aims, resources to marshal for those aims, and social structures to negotiate. Resultantly, they are more likely to take on higher risks to keep up with their competition and trust in their financial clout to weather turbulence. On the other hand, smaller household units and individual investors, wielding significantly fewer resources, suffer from cognitive and informational limitations which hamstring their decision-making, both in terms of their borrowing behaviour as well as their spending behaviour. These suboptimal decisions may have little weight on their own, but naturally such investors outnumber their organizational counterparts, and errors arising out of heuristics commonly used by people become amplified.

References

- – Agarwal & Mazumder, 2013 – Cognitive Abilities and Household Financial Decision Making

- – Bang & Frith, 2017 – Making better decisions in groups

- – Barberis & Huang, 2001 – Mental Accounting, Loss Aversion, and Individual Stock Returns

- – Brinig & Buckley 1998 – The Bankruptcy Puzzle

- – Duhaime & Schwenk, 1985 – Conjectures on Cognitive Simplification in Acquisition and Divestment Decision Making

- – Fama, 1965a – Random Walks in Stock Market Prices

- – Fama, 1965b – The Behaviour of Stock Market Prices

- – Gerardi, Moetta & Meier, 2010 – Financial Literacy and Subprime Mortgage Delinquency: Evidence from a Survey Matched to Administrative Data

- – Glaser & Weber, 2010 – Overconfidence

- – Herrmann & Wrickle, 1998 – Evaluating multidimensional prices

- – Hilgert, Hogarth & Beverly, 2003 – Household financial management: the connection between knowledge and behavior

- – Hirschleifer, 2001 – Investor Psychology and Asset Pricing

- – Janis, 1982 – Groupthink: Psychological Studies of Policy Decisions and Fiascoes

- – Kahn & Baron, 1995 – An Exploratory Study of Choice Rules Favored for High‐Stakes Decisions

- – Kahneman & Tversky, 1979 – Prospect Theory: An Analysis of Decision under Risk

- – Kamleitner, Hoetzl & Kirchler, 2012 – Credit use: psychological perspectives on a multifaceted phenomenon

- – Koop & Johnson, 2010 – The use of multiple reference points in risky decision making

- – Leith & Baumeister, 1996 – Why do bad moods increase self-defeating behavior? Emotion, risk taking, and self-regulation

- – Lord, Ross & Lepper, 1979 – Biased Assimilation and Attitude Polarization: The Effects of

Prior Theories on Subsequently Considered Evidence - Tversky & Kahneman, 1968; in Shefrin, 2009

- – Lusardi & Mitchell, 2007 – Financial Literacy and Retirement Preparedness: Evidence and Implications for Financial Education

- – Lusardi & Mitchell, 2009 – Financial Literacy among the Young: Evidence and Implications for Consumer Policy

- – Lusardi & Tufano, 2009 – Debt Literacy, Financial Experiences, and Overindebtedness

- – Malmendier & Nagel, 2011 – Depression Babies: Do Macroeconomic Experiences Affect Risk Taking

- – McArdle, Smith & Willis, 2011 – Cognition and Economic Outcomes in the Health and Retirement Survey

- – Nofsinger, 2010; in Nofsinger, 2012

- – Nofsinger, 2012 – Household behavior and boom/bust cycles

- – Peng, Miao & Xiao, 2013 – Why are gainers more risk seeking

- – Pompian, 2012; 2015 – Conservatism Bias

- – Ricciardi, 2008 – The Psychology of Risk: The Behavioral Finance Perspective

- – Rooij, Lusardi, Alessie, 2011 – Financial literacy and stock market participation

- – Rosen, 2009 – Too much right can make a wrong: Setting the stage for the financial crisis

- – Shefrin, 2009 – How Psychological Pitfalls Generated the Global Financial Crisis

- – Shefrin, 2010 – Behavioralizing Finance

- – Shiller, 2008; in Nofsinger, 2012 – The Subprime Solution

- – Stango & Zinman 2006 – How a Cognitive Bias Shapes Competition:

Evidence from Consumer Credit Markets - – Stango & Zinman, 2009 – Exponential Growth Bias and Household Finance

- Tversky & Kahneman, 1968; in Shefrin, 2009

Contact us today to discuss your finance needs.

Want one of our experts to call you?

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice.